in California, water is one of the most contested categories in insurance claims. And the main thing you need to know is that insurance companies profit from denials. This is not an emotion. It is a business model.

But California laws give you real tools to get paid. You just need to know the rules of the game.

The Main Question: Sudden or Gradual

A standard policy covers sudden and accidental escape of water.

A pipe burst under the kitchen sink. Covered.

A water heater leaked in the garage. Covered.

A washing machine overflowed. Covered.

But if the insurer decides that water was leaking gradually over a long period of time, they will deny the claim.

A real example from practice. A woman in Los Angeles noticed that the bathroom ceiling had turned yellow and slightly swollen. She called a plumber. He discovered that the shower enclosure seal had been leaking little by little for about eight months. During that time, water had soaked the framing and drywall.

The insurance company conducted its own inspection. The adjuster wrote in the report: “signs of long term moisture intrusion.” The insurer denied the claim, citing the exclusion for “continuous or repeated seepage or leakage of water over a period of months.”

Some policies even include a specific number. If water leaked for 15 days or more, there is no coverage. Even if you did not know about the leak. Even if it was inside the wall. This is called a time limit exclusion.

Another example. In Encino, a homeowner had a copper pipe burst inside the wall. Water rushed out forcefully. He called emergency services the same day. Insurance covered $18,000 in damage because the nature of the destruction showed a fresh rupture. There was no rust, no old staining.

What to do. Immediately after discovering the leak, photograph the break up close. If fresh water is visible, wet areas without signs of old rust or mineral buildup, this is evidence that the damage was sudden.

Save your water bills. A sharp spike in consumption on a specific day confirms that the rupture happened suddenly rather than slowly over years. For example, if you normally pay $80 per month and this month the bill came to $240, that is a strong argument.

Proof of Loss: The Main Document That Can Trap You

After you report the insurance claim, the company may demand proof of loss. Proof of Loss. This is an official sworn document where you describe what was damaged, when it happened, what caused it, and how much money you are demanding.

This is where the trap hides.

You are required to submit this document within 60 days from the date it is requested. If you fail to provide it, the company may claim that you violated the terms of the policy and deny coverage.

Example of a mistake. A homeowner in Burbank submitted a Proof of Loss listing damages at $12,000. But his contractor estimated the repairs at $18,000. The insurer said: you yourself valued the damage at 12, so we pay 12. And when the homeowner tried to increase the amount, the company argued that he had already provided a final sworn valuation.

How to do it correctly. You are not required to know the exact cost of repairs. The law says the burden of investigation lies with the insurer. It is enough to state: “damage exceeds $5,000,” “partial,” “known as of today.” And emphasize that you are not an expert and rely on the company’s investigation.

Another example. A woman in Santa Monica wrote in her Proof of Loss: “estimated damages not less than $10,000. Exact amount to be determined after review by an independent contractor.” The insurance company accepted the document and later could not accuse her of inflating the amount.

The main rule: do not exaggerate and do not invent. State honestly what you know. Let them investigate the rest.

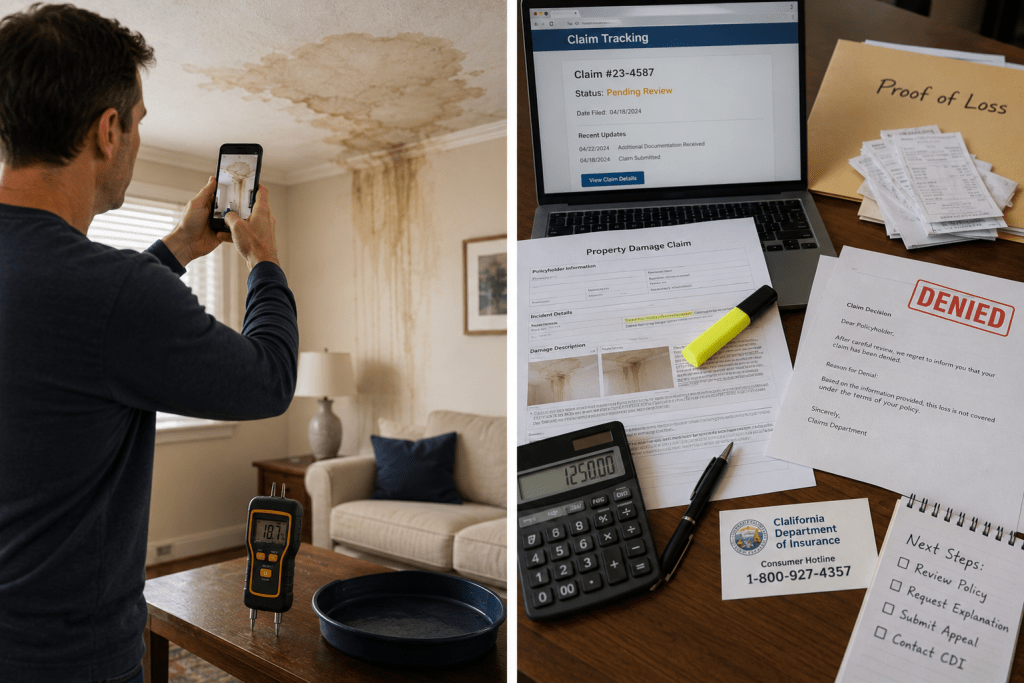

What to Do If You Were Already Denied

A denial must be in writing with a specific reason and reference to the exact policy section.

Example of a denial. “Your claim is denied under section B.2.c of your policy: damage was caused by gradual water leakage lasting more than 14 days.” This is a lawful denial if the insurer can prove it.

Example of an unlawful denial. “We deny the claim because we believe the problem was caused by pipe wear and tear.” If the policy does not contain a specific exclusion for wear and tear, such a denial may be challenged.

Step One. Do Not Believe the First Denial.

Very often, denial is a standard tactic that many people fall for. For example, the insurer may claim that water undermined the foundation from outside, therefore it is flooding, which is not covered. But if the water came from a burst pipe inside the house, that is covered. The insurer is simply trying to reclassify the loss.

A real Los Angeles case. A homeowner in Pasadena had a pipe burst beneath the floor structure. Water never surfaced, but it soaked the wooden beams. The insurance company said: this is not a sudden rupture but gradual moisture saturation, denied. The homeowner hired an independent expert who proved that the crack pattern on the pipe indicated a sudden split rather than corrosion. After a complaint to the Department of Insurance, the company reconsidered and paid $24,000.

Demand specifics. Which exact section of the policy is being used as the basis for denial?

Step Two. File a Complaint With the California Department of Insurance

This is free. CDI has a hotline: 1 800 927 4357.

CDI officers will review your complaint and determine whether the company violated Fair Claims Settlement Practices Regulations. If they did, CDI may require the insurer to reconsider the decision.

Example. In 2024, CDI received a complaint from a Woodland Hills resident whose insurance company delayed payment for a burst pipe claim three times, citing “additional review.” CDI ruled this violated the regulation requiring claims to be reviewed within 40 days. The company paid the claim within two weeks after regulator involvement.

How Independent Experts Work and Why They Matter

When you file an insurance claim, the insurance company sends its own adjuster. That person’s job is to protect the company’s interests, not yours.

Example. In Santa Clarita, after flooding, the insurance adjuster estimated damages at $8,000. The homeowner paid $500 for an independent expert. The independent estimate came back at $23,000. After negotiations, the company paid $21,000. A $500 investment produced an additional $13,000.

An independent expert works for you. They are not connected to your insurance company. They prepare their own report, which you can present to the insurer.

When this becomes especially important. If there is a dispute about when the leak began. If the insurer claims the water leaked for months but you are certain the problem appeared suddenly. An independent expert can perform diagnostic testing and issue a report that becomes your strongest argument.

How Not to Fall Into a Trap With Temporary Housing

If the damage is serious and you need to move out during repairs, your policy may cover additional living expenses.

A real example. A family in Burbank lived in a hotel for three weeks after a fire that had been extinguished with water. The insurance company paid for only 12 days, claiming repairs could have been completed sooner. The family filed a complaint with CDI and received compensation for all 21 days because the contractor confirmed the actual repair timeline.

What you need to know. You are not required to stay in the cheapest hotel available. Policies usually require that expenses be reasonable. But “reasonable” does not mean “minimal.” If you are accustomed to living in a home with a kitchen and laundry, and the hotel lacks those amenities, you may request reimbursement for renting an apartment with a full kitchen.

Keep all receipts. Hotel, food, laundry. All of it may be included in coverage.

When the City Is Responsible

Sometimes the water comes not from your pipes but from city infrastructure. A LADWP main line break. A municipal sewer backup. Water line damage during road work.

An example from West Hollywood. In 2023, a city main line burst and flooded the basements of 8 homes on one street. Residents filed a collective claim. Each received between $5,000 and $12,000 from the city.

Important deadlines. You have only 6 months from the date of damage to file a written claim with the Los Angeles City Clerk’s office. Miss the deadline and your right to compensation is lost forever.

The city has 45 days to respond. If the city denies your claim, you have another 6 months to file a lawsuit. If the city does not respond within 45 days, the claim is considered denied, and your 6 months to sue begin from that moment.

These deadlines are absolute. A one day mistake can destroy your right to compensation.

Mold: The Most Disputed Issue

Mold creates the biggest disputes in California insurance claims.

Example. A homeowner in Pacific Palisades had a pipe burst inside a wall. He called emergency services. The water was removed the same day. Two weeks later, mold appeared on the wall. The insurance company initially refused to pay, arguing that mold was excluded from coverage. The homeowner filed a complaint and won because the mold arose directly from the covered leak. Without the pipe burst, there would have been no mold.

The opposite example. In Malibu, a homeowner had a bathroom sink slowly leaking for years. He ignored the odor and minor drips. Two years later he discovered a massive mold patch behind a cabinet. Insurance denied the claim. And correctly so. The mold resulted from long term neglect, not a sudden covered event.

Mold is covered only if it arose directly from a covered leak. And you reported the problem quickly. And you acted reasonably to stop further growth.

How We Help With Your Insurance Claim

We handle the damage and we handle the paperwork so you can focus on your life. We work directly with your insurance company, including State Farm, Allstate, Farmers, AAA, Mercury, Nationwide, Liberty Mutual, Travelers, The Hartford, Chubb, USAA, and all other major carriers. Our team provides complete insurance claim support: free on site inspection and moisture mapping, thermal imaging, direct communication with your adjuster, full documentation packages with drying logs and moisture readings, and direct billing to your insurance company so you pay nothing out of pocket except your deductible.

Оставить комментарий